.png)

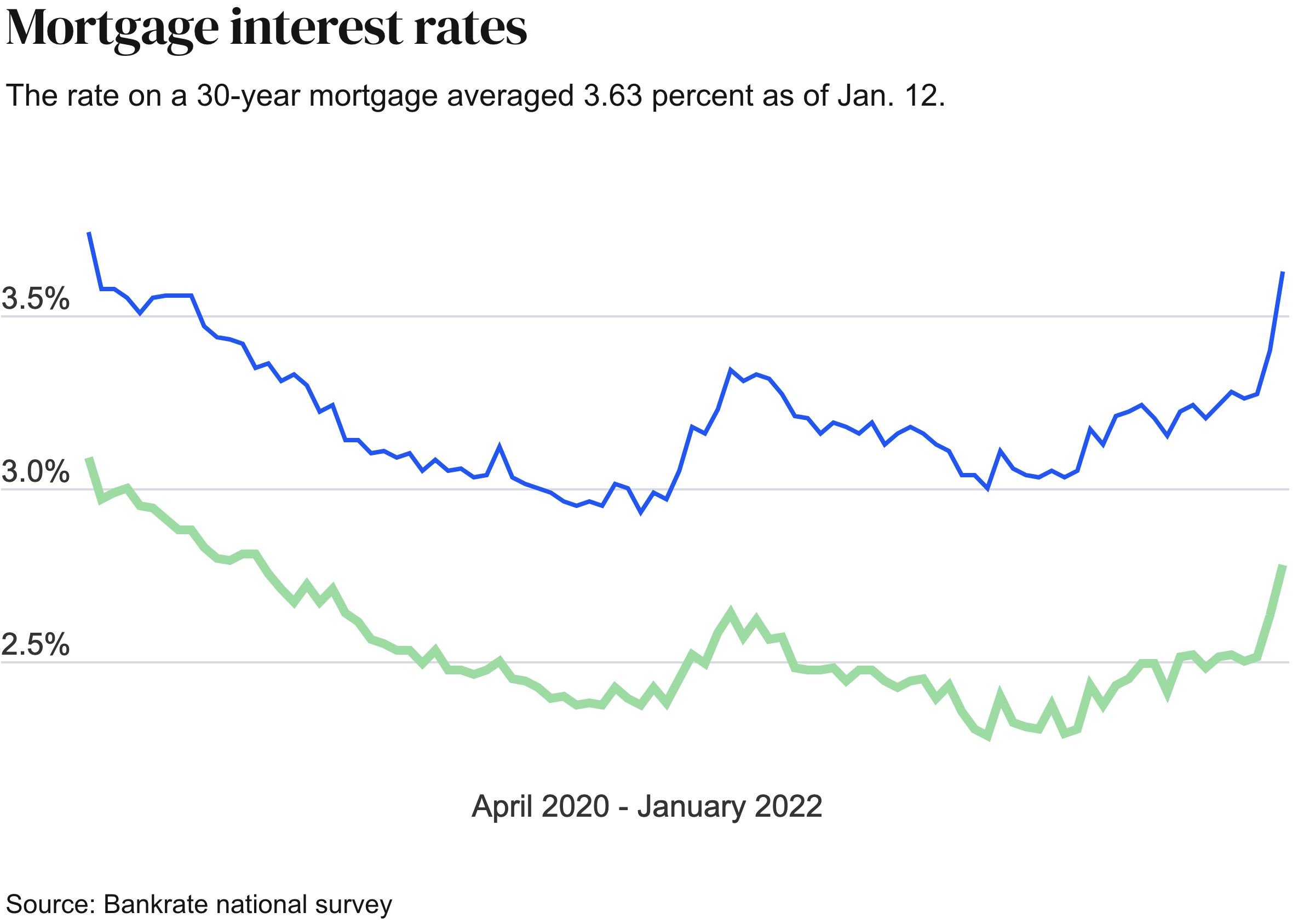

If you follow the news, especially in the financial sector, you saw that mortgage rates increased last week. According to Bankrate's weekly poll of large lenders, the average rate on 30-year mortgages increased to 3.85 percent from 3.76 percent last week. Experts predict that rates will continue to rise from their all-time low of 2.93 percent in January 2021. The benchmark 30-year fixed-rate mortgage was 2.97 percent a year ago. The rate was 3.63 percent four weeks ago. For this week, the 30-year fixed-rate average is 0.92 percentage points higher than the 52-week low of 2.97 percent.

The Labor Department reported last week that inflation for the 12 months ended in January was 7.5 percent, the fastest year-over-year rate since 1982. Even when volatile food and energy prices are excluded, core inflation increased by 6% in the past year. That was also the most significant increase in four decades. And the Federal Reserve has indicated a hike in interest rates is coming, possibly as soon as March 2022.

So How Does This Affect Homebuyers?

Simply, borrowing becomes more expensive when interest rates rise. For consumers, this could entail higher mortgage expenses, albeit the impact would not be felt right away for the vast majority of homeowners, and some will be exempt entirely.

Fixed-rate and adjustable-rate mortgages are the two most common mortgage loans, with hybrid variations and various derivatives of each available. A fundamental grasp of interest rates, as well as the economic factors that influence their future direction, can assist you in making financially sensible mortgage selections. Choosing between a fixed-rate mortgage and an adjustable-rate mortgage (ARM) or refinancing out of an ARM are two examples.

What Can You Do About It?

Because of the increase in rates, borrowers have to work harder to maintain their payments within their budgets. However, it's vital to keep in mind that interest rates are still low by historical standards. For individuals looking for a new mortgage, a refinance, or a cash-out refinance, here are a few wise ideas to consider:

- Shop Around

Compare at least three mortgage offers to determine the best plan for you and your family. Rates and fees differ between lenders, and consumers who shop around can save thousands of dollars over the life of the loan. - Maintain a High Credit Score

The single most crucial element affecting the mortgage rate and terms you can get is your credit score. Therefore making payments on time can have a direct impact on your score. Be sure your payments are timely and if you can, pay down any debt sooner by paying more than the required monthly payment. - Paying Points

Mortgage points are expenses paid to a mortgage lender in order to lower the loan's interest rate. According to mortgage data provider Black Knight, as rates have risen, more borrowers are paying points to get a better interest rate.

Additional Thoughts

If you’re hoping to purchase a home this year and you’re not up to speed on the process, not sure if you’re in a good position to do so, and wonder your credit score is up to snuff, it may be time to find an agent and a lender to help you analyze your situation and make a plan. Both are excellent resources, especially if you find highly-experienced people. The Mountain Life Team strives to make the process easy to understand, transparent, and as smooth as possible to help you and your family realize your dream of buying a new home.

Our buyer’s agents will be by your side throughout the entire home buying process. We will provide you with the knowledge and insight you need to make informed decisions, and will take care of all contingencies required throughout the process. In an effort to make things as easy as possible for you, we’ll mediate any important conversations all the way through closing. We work hard, so you can enjoy the excitement around buying your dream home. We’re here when you’re ready and would be humbled to work with you and your family.

.png)

Footer Social Links